The Future of Physical AI is Built on Human Data: Our Investment in mimic

Since launching our first industrial tech fund in 2018, we have witnessed several eras in the robotics landscape. Yet in these seven years, the industry has never felt more ready to explore and adopt new solutions than it does now. Over the past two decades, robotics has evolved from pre-programmed factory automation to collaborative cobots and AI-driven perception. Today, industrial installations are up more than 2x than 10 years ago & embodied AI has reached an inflection point, enabling robots to tackle a new set of tasks that were previously extremely difficult, at least in labs.

Now, the next frontier is learning-based autonomy: robots that continuously adapt, generalize, and collaborate across dynamic environments. One of the teams that is leading the charge is Zürich's mimic Robotics. We’re incredibly proud to invest in their $16 million Seed round and want to use this opportunity to share our thesis on why we are bullish about Europe’s robotic opportunity.

Imitation Learning to Unlock Dexterous Automation at Scale

Mimic builds frontier physical AI models trained on real-world human demonstrations, using proprietary data collection devices that operators are wearing while performing their daily work on factory floors to overcome the data scarcity problem. In practice, this means dexterous robotic hands that can perform complex tasks previously impossible for traditional automation, such as tool handling, pick & place, and precision assembly, paired with industrial robot arms.

By pioneering this imitation learning approach, mimic’s systems can autonomously adapt to changing environments, handle disturbances, and self-correct. Ultimately, when looking at the market opportunity, this proprietary data acquisition and training approach means that mimic is competitive at the robot foundation model layer as well as the vertical application layer.

What excites us most about the company, however, is how they build trust with their customers and end-users through their approach. Lack of trust, risk aversion, and cultural caution are some of the main reasons why industrial enterprises and SMEs in Europe often shy away from deploying new, intelligent systems. After all, new scientific discoveries, by themselves, are far from offering solutions to real-world problems. mimic found its way in by offering this tangible training approach that engages employees and allows them to understand the black box that autonomous systems often are for them. In summary: Easily understandable from the outside, with frontier research on the inside.

We’re proud to be a part of mimic’s latest funding round and look forward to supporting this world-class team around Stefan, Stephan-Daniel, Elvis, Benedek, and Robert as they scale their unique hardware and software.

Europe has the talent, the infrastructure, and the demand, and mimic is building the company that brings all of this together. After our first 30-minute call, it was quite clear that they fit perfectly into our wider thinking on Europe’s role in the future of robotics.

Does Europe have a chance in the robotics race? Yes, big time!

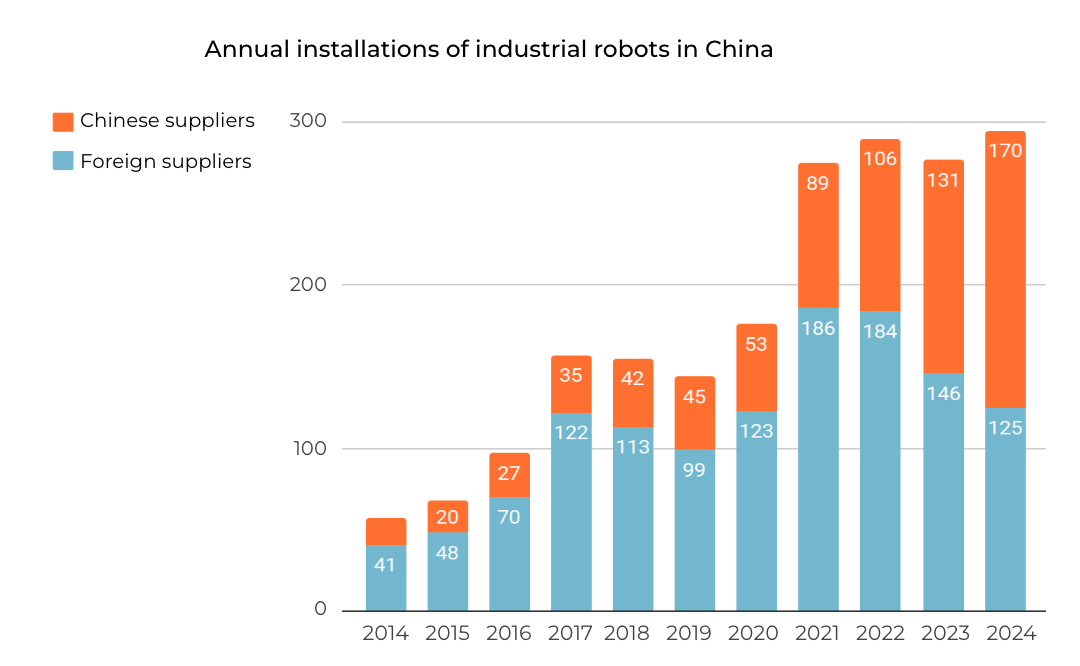

Softbank’s recent acquisition of ABB’s Robotics Business was described by many as Europe’s defeat in Physical AI. While losing one of the big four industrial robot companies to Japan (with the other two being Japanese as well) is unfortunate, and China leading the annual installation game by an overwhelming absolute volume (see below) is daunting, some facts keep us optimistic: While China is with no doubt the largest market, over 40% of these installations in 2024 were still imported by foreign suppliers, according to the International Federation of Robotics. With >50% and $3 billion in shipment volume, Europe is the biggest exporter by continent.

This also means that most European-manufactured robotics systems (from firms like KUKA, Universal Robots, Comau, and others) are primarily deployed within Europe, especially in Germany, Italy, and France. From the precision engineering hubs of Germany and Switzerland to Scandinavia’s sensor and actuator clusters, the continent hosts some of the world’s most advanced industrial automation ecosystems. European suppliers have quietly shaped global production standards for decades, providing the mechanical, electronic, and systems foundations that modern robotics now builds upon.

These numbers spur our optimism: Europe doesn’t only have an edge, but also a structural advantage.

Robotics advancement is happening on two closely interlinked fronts: development and implementation.

On the development side, the primary factors to consider are talent and research: Europe boasts unmatched talent density and research excellence. Five of the world’s top ten technical universities are European, producing more than 1.3 million STEM graduates annually, around 60 percent more than in the U.S.

These talents have learnt at some of the leading robotics research institutions, such as the ETH, TUM, TU Delft, and EPFL, and are supported by Europe’s deep applied engineering culture. Countries like Germany have a strong history of promoting Applied Research Institutes like Fraunhofer that strongly push innovations to the factory floor. This has enabled some ground-breaking technologies we are using every day, such as the airbag and solar panels.

On the implementation side, our deep industrial base provides natural testbeds across some of the core application fields of robotics: automotive, industrial machinery, logistics, and construction. This proximity to real-world use cases is gold, as we’re actually speaking about interacting with the physical world here, compared to companies working on the software side of AI. Also, when looking at relative numbers, Europe has the highest average robot density (robots per 10,000 employees) on a continent level.

Policy and labour market developments further strengthen this position. Structural labor shortages, aging workforces, and EU programs like Horizon Europe and IPCEI are channeling funding into robotics R&D and digital infrastructure. Europe’s emphasis on strategic autonomy, reindustrialization, and the green transition makes robotics both an economic and political priority.

Scalable Intelligence as an Equation of Data & Economics

This research excellence and application playground now needs to be translated into globally competitive commercialization. When addressing the topic of robotics with our industrial LP base, it becomes clear very quickly that there is still a huge gap between what works in the lab and what works in the factory or the warehouse (and likely also at home - we’ll know soon after pre-ordering 1X’s Neo).

One of the core reasons for this is that true robotic intelligence still depends on data, but today’s training pipelines are often still task-specific, super expensive, and brittle. Collecting high-quality data for robotic learning is time-consuming and highly contextual. What works for one task, object set, or lighting condition often fails elsewhere. Simulation helps, but sim-to-real transfer remains a persistent challenge: models trained in virtual environments often underperform in the messy, unpredictable physical world. Unlike in computer vision or NLP, robotics still lacks shared standards, benchmarks, and open datasets, which limits collective progress. Every team is effectively rebuilding the data flywheel from scratch, still slowing down learning-based autonomy at scale. Mimic directly addresses this bottleneck by capturing real-world human demonstrations to build scalable, transferable data pipelines - turning the physical world itself into a training set for robotic learning.

Another central issue: for many robotics startups, unit economics don’t work out. Customers are not used to the RaaS (Robotics-as-a-Service) business models, and would prefer to own their equipment in-house. Utilization, maintenance, and integration costs vary widely by customer environment, which makes it difficult to demonstrate a clear ROI. In practice, this leads to many teams being stuck in integration projects and long sales cycles. On top of that, many industries have burned money & effort on previous automation integration projects that didn’t deliver the payback they were hoping for. All of this is exactly why we’re excited about learning-based robotics models, such as Mimic, gradually making their way into industrial environments. Mimic has already shown early success cases where its systems take on entirely new customer tasks with incredible speed and at costs increasingly competitive with human workers - an important signal of how imitation learning approaches can unlock scalable, general-purpose automation.

Our hunt for the next European robotics play doesn’t stop here

Internally, we think about robotics companies within the following three categories: (1) Foundational Enablers, (2) Learning Models & Autonomy Stack, and (3) full-stack vertical platforms (Mimic sitting across #2 and #3).

Category 1 is like the cloud infrastructure and DevOps stack for robotics. It is naturally not the tech that is pioneering a field, but 10x-ing its scale-up. A core part of it is the infrastructure layers where data is generated, labeled, and processed, the backbone for scalable learning. We’re thinking of simulation, motion planning, and orchestration platforms, but also IoT security, hardware engineering, and data visualisation players.

Category 2 represents the heart of where innovation is currently happening on the research side: imitation, simulation, and reinforcement learning approaches, integrated with perception, reasoning, and planning systems. The holy grail is obviously foundation models for robotics and new ways to unify perception with control across any thinkable use case.

Category 3 describes the applications and platforms that leverage these capabilities in high-impact domains, from manufacturing and logistics to construction, agriculture, and defense. These vertical champions turn autonomy into real economic and operational value, while often owning parts of category 2 in-house as well (keyword data flywheel).

We love founders who combine technical depth with a scalability-obsessed mindset:

- Access to proprietary datasets or domain models that improve performance

- Deep research and developer traction, through publications, active repos, or university networks

- A clear path to Robotics-as-a-Service (RaaS) or API-based monetization, rather than project-driven service revenue

We’re excited to see and witness robotic deployments move beyond deterministic control into adaptive, learning-based autonomy. In companies like mimic, we see a founding team that understands and is set to scale beyond existing market paradigms. Because those who can build the data and learning layers beneath this shift, not just the machines, will shape the next industrial revolution.

.svg)