This blog is part of Speedinvest’s data-driven blog series Digital Health in Europe: A Data-Driven Blog Series by Speedinvest. We outlined in the series’ opener why and how we’re systematically mapping out the ecosystem.

TLDR: As one of the most active investors in early-stage Digital Health in Europe, we’re surprised by how little data there is on this fast-growing vertical. This series aims to change that.

At Speedinvest, we think we’re on the cusp of a golden decade of Digital Health in Europe and want to share the reasoning behind our conviction. Our goal for this blog is to bring facts and data to the conversation about Digital Health. It draws on a comprehensive database we assembled, covering 626 Digital Health startups founded in Europe in the last decade, to provide insights on:

- Overall startup activity in European Digital Health

- Regional differences and characteristics

- Funding levels and trends

- Sub-verticals and trends within Digital Health

If you’d like to join the conversation as well, drop me an email or get in touch on Linkedin, but most importantly, read on!

Related Reading: Top Early-Stage European Healthtech VC Funds

The data

Here is a detailed background post on the data and methods we used. Our analysis started with a data export of 1599 companies from Dealroom’s startup database. We narrowed and augmented that to 626 companies by focusing exclusively on software companies that:

- work on human health,

- have received funding and

- are still operational.

While our data is far from perfect, it represents a large enough sample to draw valuable insights, which we’re summarizing below.

Sizing the ecosystem: 626 companies, ⅔ younger than 5 years, growing fast

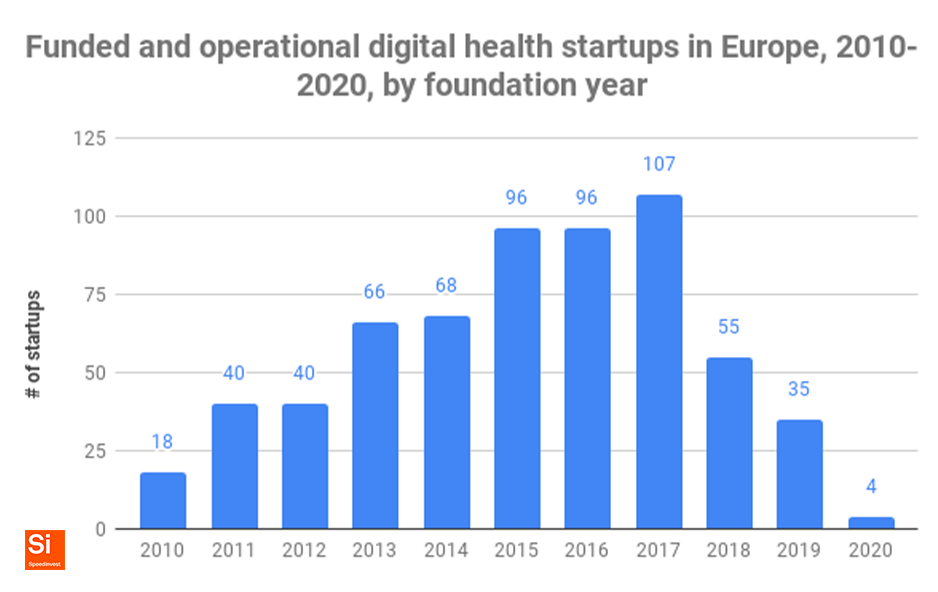

There are 626 funded Digital Health companies active across Europe today, including 18 startups founded in 2010 and 106 from the 2017 cohort. The numbers for 2018–2020 drop off because a lot of companies’ funding rounds have not yet been recorded (the reporting lag) or they have not raised funds yet. Note that >63% of funded Digital Health startups in Europe were founded in the last five years. This is an extremely young sector.

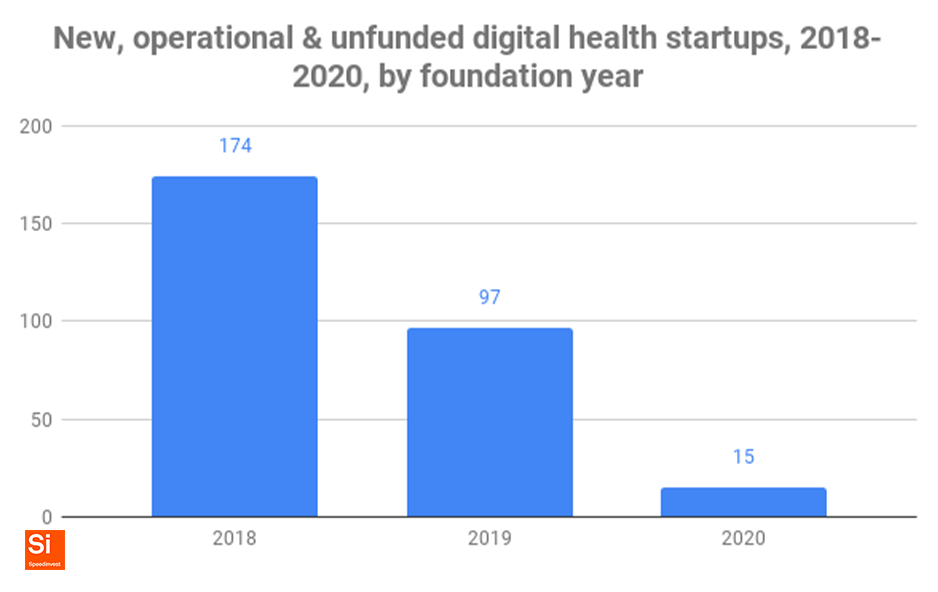

If we include unfunded startups founded in 2018–2020, below, we see further evidence of strong growth; 174 Digital Health companies were born in 2018 alone.

In case you’re wondering, simply adding these charts is not useful. To align these two types of data (funded vs. unfunded companies) we would have to factor in how many unfunded startups will cease operations and how many will receive funding. Instead, we looked at another proxy indicator: our CRM. It shows that in 2019, we looked at a whopping 436 Digital Health companies. In the first three quarters of 2020 alone, this number was 381.

It’s safe to say the ecosystem is growing fast. Given its young age, it’s no surprise that zero Digital Health companies made it onto Accel’s 2020 Euroscape of the Top 100 software companies. It takes companies on that famed list a median of six years to make the cut, and only 68 companies from the 2014 batch are still around today to try.

On the upside, Accel’s “Champions League” of high-growth, category-defining unicorns includes one health company (congrats, Doctolib). A small number, but proof that there is potential for growth.

Summing up, the European Digital Health ecosystem is young and growth has accelerated rapidly in the last three years. We expect 5–10 Digital Health companies on the Accel Top 100 by 2025.

Geo-distribution: UK leads the pack, but talent lurks everywhere

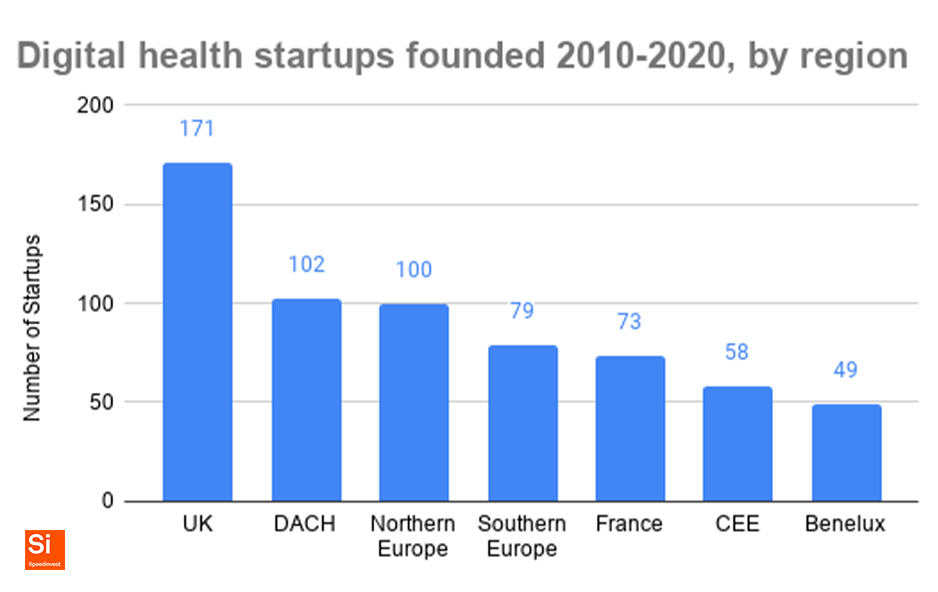

We also analyzed the regional distribution of Digital Health companies across Europe (loosely following the EuroVoc standard). The result: the UK is the clear Digital Health leader of the last decade, followed by DACH and Northern Europe. France is the second largest single national market, followed by Germany.

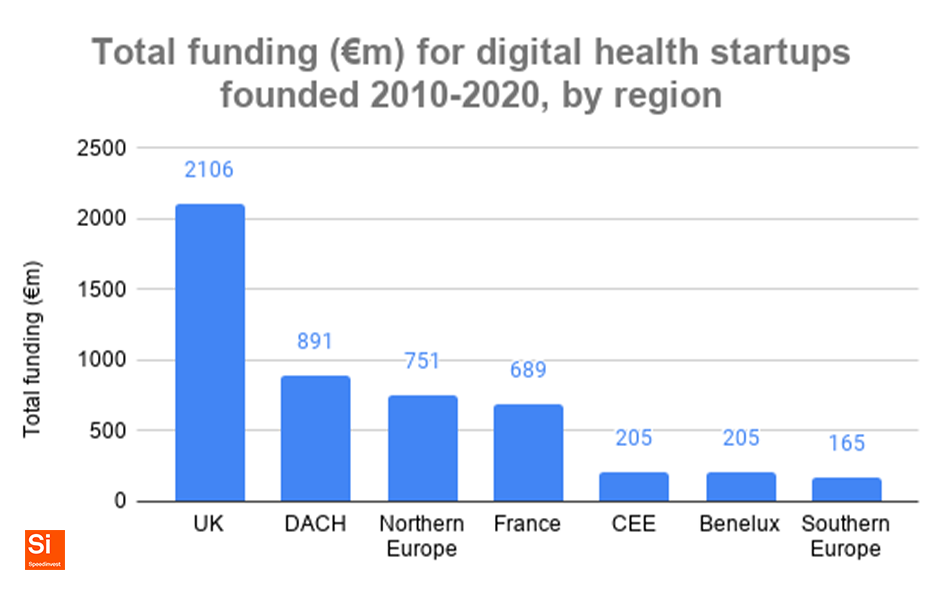

Funding by geographies: three blocs with very different market capitalization

A look at the regional distribution of Digital Health funding over the last decade shows three distinct blocs of capitalization:

- The UK is a highly capitalized market, with 2x the total investment of the runner-up region, DACH;

- DACH, France and Northern Europe are midfield markets, with similar total funding levels;

- CEE, BeNeLux and Southern Europe are laggards with very little Digital Health funding.

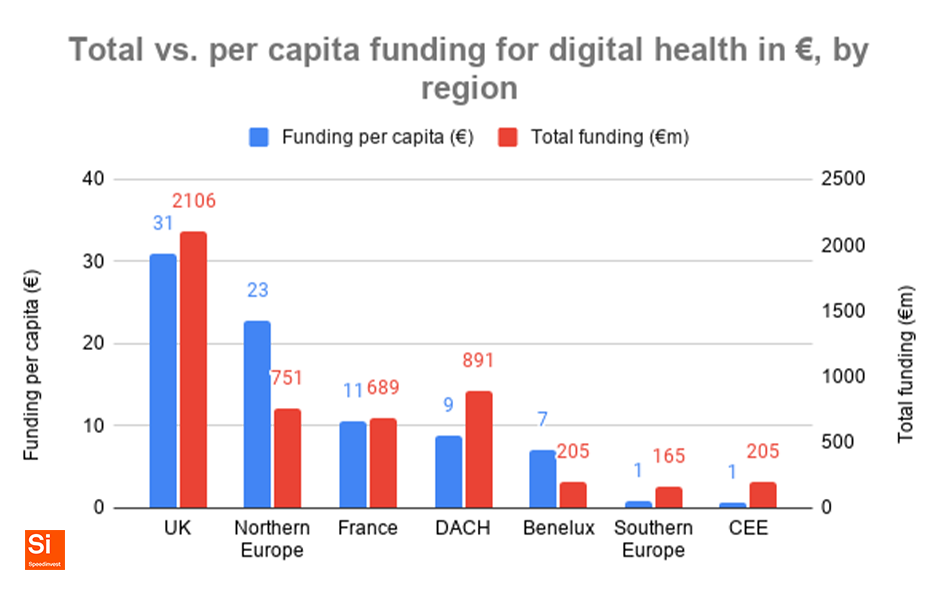

Are the different funding levels simply due to different market sizes? A look at per capita funding (funding relative to a region’s population) doesn’t confirm this:

- The UK is still the clear #1;

- Northern Europe is punching above its weight and comes second in per capita Digital Health funding;

- France, DACH and the BeNeLux countries form the midfield;

- Southern Europe and CEE are undercapitalized.

We learned two things from this regional analysis:

- First, talent and opportunity comes from anywhere. As if to prove this point, two big Digital Health Series A rounds in 2020 came from underrepresented markets: Infermedica from Poland (also home to scale-up Docplanner) and Siilo from the Netherlands.

- Second, assuming our first learning holds, there is lots of opportunity waiting to be uncovered in undercapitalized markets like Southern Europe, CEE and BeNeLux.

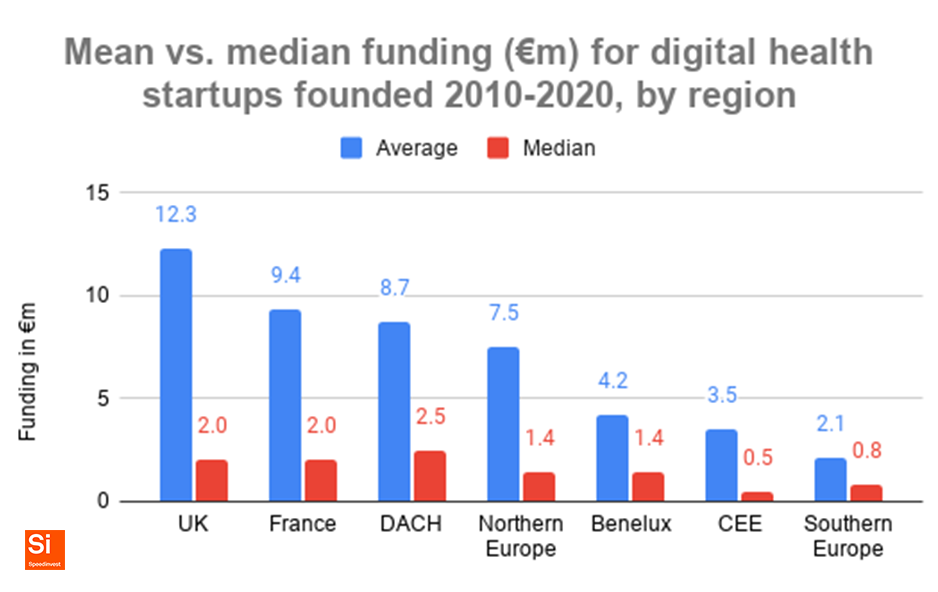

Funding per startup: median funding high in DACH, low in CEE/Southern Europe

A more granular analysis of total funding per startup across regions shows an even more nuanced picture:

- On the one hand, average funding per startup in each geography closely tracks total funding in that region, a result driven by large rounds in highly capitalized markets (e.g. Babylon in the UK or KRY in Sweden).

- On the other hand, median funding per startup is broadly similar across all geographies.

- Exception 1: Median funding per startup in DACH (€2.67m) is higher than anywhere else, including 42% higher than the UK’s (€1.92m).

- Exception 2: Median startup funding in CEE and Southern Europe is extremely low.

Of course, averaging values over a 10 year period (or seven year period actually, as there are few post-2018 rounds in the dataset) doesn’t account for valuation growth in that time, but we find the patterns described below are in line with our market experience.

(Source: Speedinvest using data from dealroom.co)

What founders like: B2B, hardware-heavy, still avoiding patients

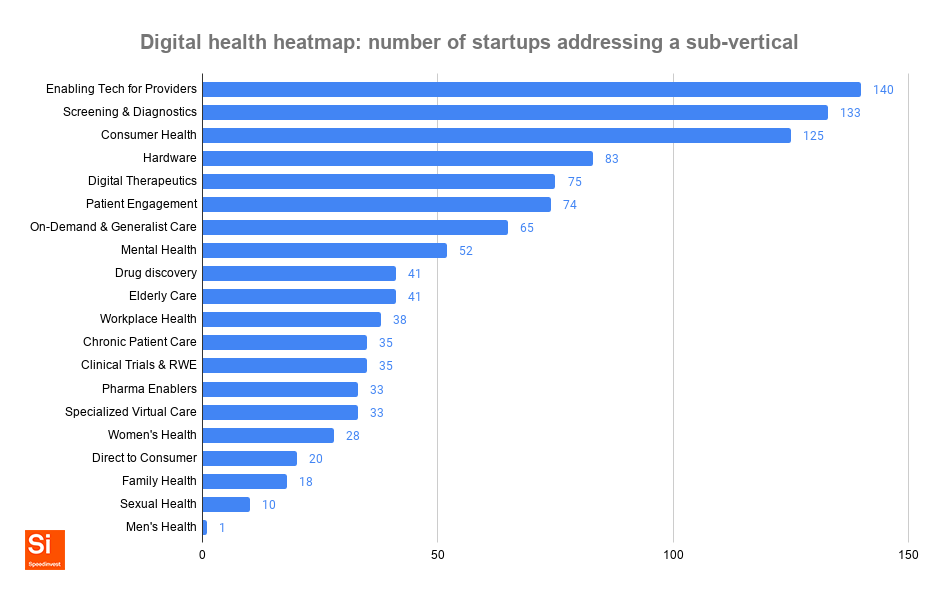

“Digital Health” is not a vertical, it’s a collection of verticals. So we decided to map topics or sub-verticals they work on. In the first step, we assigned tags based on all relevant categories in which a startup operates (i.e. companies got tagged for multiple topics). The result is a heat map that shows which topics are hot in Digital Health in Europe (here’s more on our method and why we use these buckets).

- The #1 category is enabling tech for health providers, software that supports providers with their daily workflows via software that is focused on back-end, and business process tools for health providers. Outside of Digital Health, this would be B2B SaaS. Examples: Pando (UK, medical communications), Doctorly (Germany, practice management software), Awell Health (Belgium, pathway management for hospitals).

- The #2 focus area is tools for screening and diagnostics, a broad bucket that includes some B2C home testing but predominantly involves B2B software for various diagnostic use cases, such as AI for pathology or radiology images. Examples: Bioserenity (France, remote diagnostics platform), DeepSpin (Germany, AI-powered miniature MRI), Quibim (Spain, radiology AI).

- Consumer health apps are the third largest category and mostly involve consumer apps for well-being and nutrition advice. The size of this basket is surprising given how hard it is to monetize in Europe and how few success stories there are (see below). Examples: Second Nature (UK, weight loss app), 8fit (Germany, nutrition and lifestyle advice), Oura (Finland, sleep tracking).

- Pharma-related software is a broad field that we’ve disaggregated into “Drug Discovery” solutions, often Deep Tech/AI applied to molecular modeling, ”Clinical Trials” solutions that provide access to trial patient data or real-world evidence, and “Pharma Enablers” that focus on non-clinical problems in the life science industry. Taken together, this is a very mature field in European tech. Examples: Nightingale (Finland, blood testing and research), Benevolent (UK, AI for drug discovery), Inato (France, clinical trial platform).

- A high share of hardware startups reflects that, across all of these categories, many startups opt for a combined software + hardware strategy, in areas as disparate as diabetes care and sexual wellness.

- Even though direct patient care, such as chronic care or specialized virtual care, represents a huge share of public and private wallets in the offline world, a surprisingly small number of companies are taking on these areas and are also far more mature in the US.

- Largely underexplored spaces include Men’s Health, Sexual Health and Family Health. Noteworthy examples include: Numan (UK, men’s health), Blueheart.io (UK, sex therapy), Emjoy (Spain, intimate wellbeing for women).

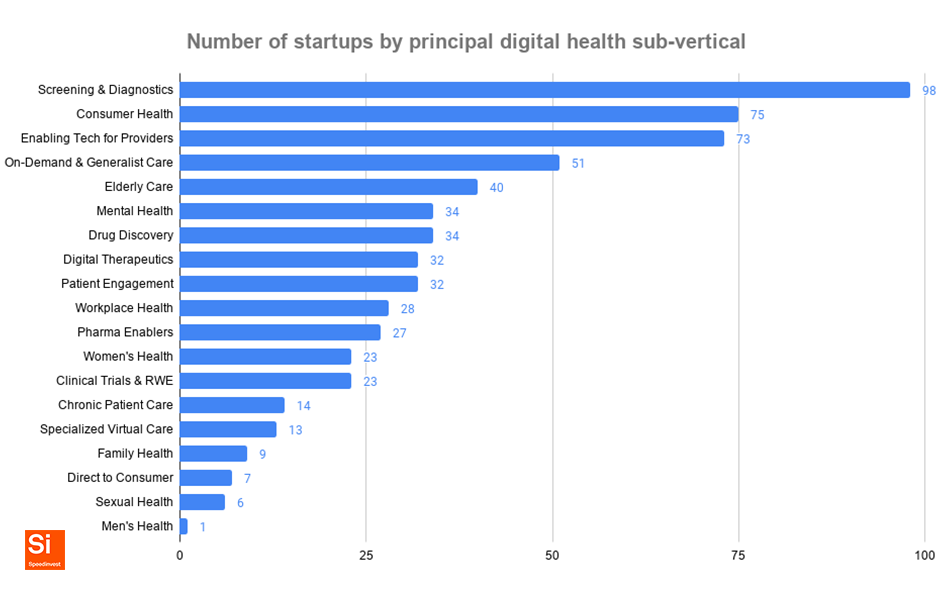

To be more specific about startups’ main focus areas, we additionally assigned a primary tag to each that describes its principal use case. The result is a slightly different lens through which to examine which Digital Health sub-verticals have received the most attention from founders.

- Screening & Diagnostics, Consumer Health and Enabling Tech remain the most prevalent focus areas in our database, though in a slightly different order. This is mainly because many startups build some “enabling tech” even if they pursue a more focused strategy.

- On-demand Generalist Care (a.k.a. telemedicine) pops up as a fourth big focus area, and we expect this to accelerate as a result of COVID-19. The increased importance is a result of many telemedicine providers having an additional focus in the earlier chart (e.g. telemedicine for kids, diagnostic support, mental health, etc.).

- Mental Health & Elderly Care become more prominent focus areas, a trend that we expect to see more of in the years to come given an aging population and the pandemic-induced mental health crisis.

- Hardware drops out by default, as we’ve excluded traditional medical device companies.

What investors like: on-demand care, provider tools, deep research and funky hardware

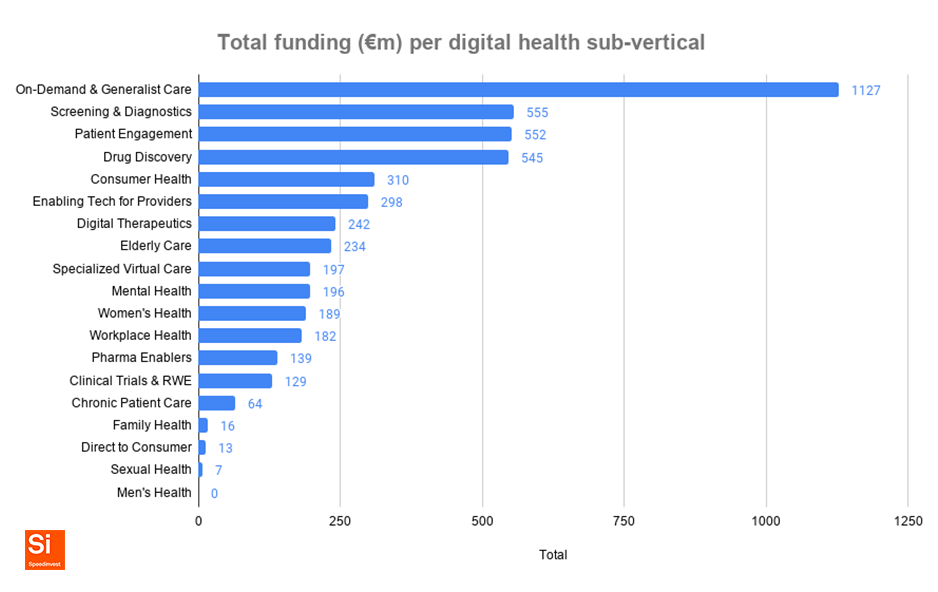

We’ve seen what European health founders like building. Here’s where investors have put their money:

The above look at total funds raised per sub-vertical shows that:

- Funding, generally speaking, tracks with the number of startups per sub-vertical. This makes sense; more funded companies in a niche means more funding for that niche.

- On-Demand & Generalist Care is a massive outlier, a result driven by the €577 million raised by Babylon Health and Kry’s €227 million in funding.

- If we were to group Drug Discovery, Clinical Trials & RWE and Pharma Enablers into one broad category of “software for life sciences”, this would be the clear #2 category by funding, totaling €813 million. We’ve broken them down here, but it’s important to keep in mind how much investor appetite pharma related industries receive.

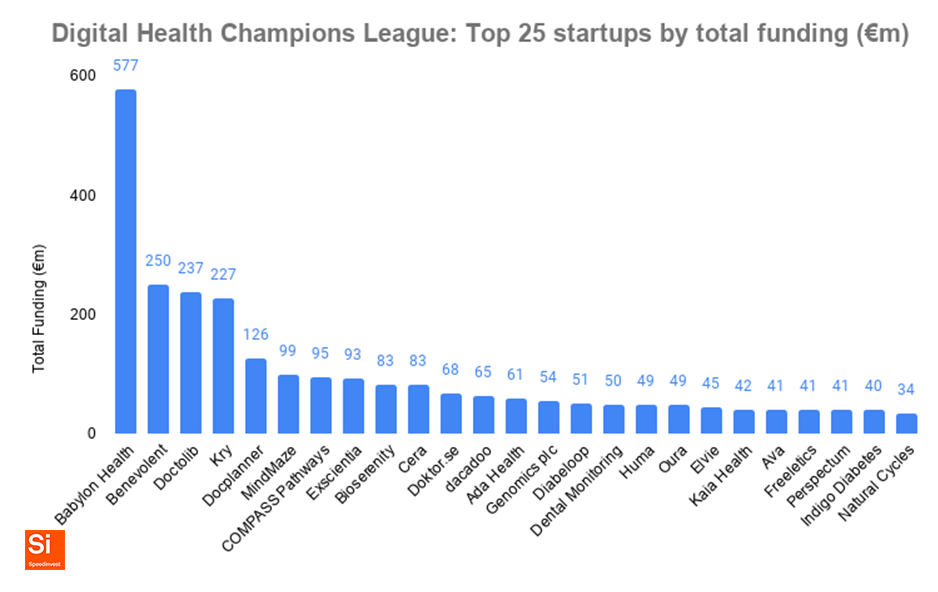

Since the above funding amounts — and VC returns — are driven by outlier events, it’s worth taking a closer look at the 25 top funded companies in Digital Health.

What we see is:

- The top five most funded companies come from five different countries, the top 25 from seven. Great companies come from anywhere.

- The largest rounds have been raised by On-Demand & Generalist Care players like Babylon, Kry, Doktor.se and Ada, as well as Patient Engagement solutions like Doctolib and Docplanner (which are also enabling tech for providers; we figured that their patient-facing business models are key value drivers).

- Drug Discovery tech attracts very big funding rounds, as evidenced by second-ranked big data behemoth Benevolent, as well as large rounds raised by Exscientia and Genomics. Digital health companies with biotech-like R&D pipelines and highly specialized propositions in the neuroscience space, such as Mindmaze (that also provides specialized virtual care) and Compass Pathways, have also attracted significant funding.

- Early leaders in Women’s Health hardware have raised large rounds, specifically Ava (€41m, fertility tracking wearables), Elvie (€45m, digitally enhanced breast pumps and pelvic trainers), as well as Natural Cycles (€34m, birth control)

- Further to the right, startups like Kaia, Diabeloop or Indigo Diabetes prove that Digital Therapeutics as well as Specialized Virtual Care also attract significant funding — but are less capital intensive and therefore don’t need extreme raises like Kry and co.

- Interestingly, health-focused AR/VR solutions like Dental Monitoring (for dental) and Mindmaze (for neurological applications) have attracted significant capital.

- Hardly any Consumer Health companies in the Top 25, only Freeletics and Oura’s sleep tracking ring (which seems to be heading down a more medical road) make the cut.

What founders should expect: few raises above €2 million

We often get asked by founders how much they should aim to raise. There’s no easy answer, but the data suggests that few companies will raise beyond €2 million. Beyond the outliers discussed above, the average and median funding data below is a more realistic perspective on each subvertical. While average funding is still driven by large rounds, median funding gives a more realistic picture of how much startups in these fields have been able to raise in total over the past decade (across all stages, from pre-seed to Series D+):

Some interesting observations:

- Most median funding amounts are between €1–2 million. That is, most companies raise very little money.

- Specialized Virtual Care has the highest median funding per startup (€5.7 million, more than 2x that of next-ranked elderly care) due in part to a smaller sample number (n=12), but also due to fairly large fundraises in that category by Current Health (€21m, remote care), Joint Academy (€11.5m, MSK support), Oviva (€34m, nutrition tracker), Quit Genius (€12m, smoking cessation) and Mindmaze (€98m, tele-rehab für neurological conditions).

- Elderly Care (sample size n=36) ranks fifth by median funding (€1.9 million) thanks to 10 companies that have raised between €4m and €20m, such as Care Sourcer (€12.6m), Elder (€17.9m) and Safe365 (€5m). The category also includes a Top 25 company, Cera Care, who have raised >€80m for tech-enabled elderly care.

- It’s good to see that Women’s Health (sample size n=23), still a nascent field, ranks 3rd by median funding and 4th by average funding. This result is driven by three hardware-focused players Ava, Elvie and Natural Cycles. But from our own deal flow we know there are some strong companies in earlier funding stages.

- Mental Health startups have received high average funding (€5.8 million) but very low median funding (€1 million). It’s a popular space among founders (33 startups in our database and growing fast in 2020), which leads to intense competition and a concentration of funding on a few winners like Compass Pathways (€95m raised). Mindmaze (€98m) could also be placed in this category.

- Likewise, Consumer Health ranks #2 by number of startups in the heatmap (125 total) and #3 by principal focus area, but is in the bottom third of median and average funding. Lots of competition in this segment, and difficult to get funded.

Conclusions

We’ve covered a lot of ground in this blog but we feel we’ve only scratched the surface. Here are our key takeaways:

- Digital health in Europe is only getting started. Most company formation has only been happening in the last five years and several of the top-funded business models are, let’s be honest, fairly simple. A golden decade lies ahead!

- Plenty of white space for founders away from the crowds. We’d love to see founders tackle topics outside of crowded trends in consumer health or B2C mental health apps.

- Huge opportunities for investors outside the hubs. The top five most funded health companies come from five different geographies. VCs focusing only on the hubs will miss great opportunities.

- European Digital Health is predominantly a B2B market. We know from our daily work that B2B go-to-market and sales acumen decide the day. Health founders need to double down on this skill set.

- Breakout success is rare. A lot of companies never raise significant funding, even though they build valuable companies, have great intellectual property and do important work. We have incredible respect for everyone who tries to make it. Thanks for your hard work.

We hope you’ve found this blog useful. Drop me an email or get in touch on LinkedIn if you’d like to share feedback, ideas on how to improve, or just want to nerd out on Digital Health. Also, stay tuned: Next up are regional deep dives based on our awesome database.