This blog is part of Digital Health in Europe: A Data-Driven Blog Series by Speedinvest. We outlined in the series’ opener why and how we’re systematically mapping out the ecosystem. TLDR: as one of the most active investors in early-stage digital health in Europe, we’re surprised how little data there is on this fast-growing vertical. We want to change that.

Inside our European Digital Health database

We’ve built Europe’s most comprehensive and detailed digital health dataset. If you made it down here, congratulations: You’re certified a digital health nerd! You should get in touch about funding or apply for a job at Speedinvest or our portfolio companies here. Meanwhile, this blog outlines the data behind our Digital Health in Europe blog series, what startups we included and excluded, and how we categorized all the startups in our dataset.

At the risk of stating the obvious, our analysis is informed and shaped by our perspective as pre-seed and seed investors in digital health startups that build software for health.

We tried to strike a generous balance between being comprehensive (including all relevant companies) and pragmatic (excluding companies we consider far outside our investment scope). Our database does not aim to provide a comprehensive overview of the entire health ecosystem in Europe, which extends far beyond the world of digital health startups.

We’re sharing our method here to be transparent, encourage critical feedback and improve future iterations.

Data extraction

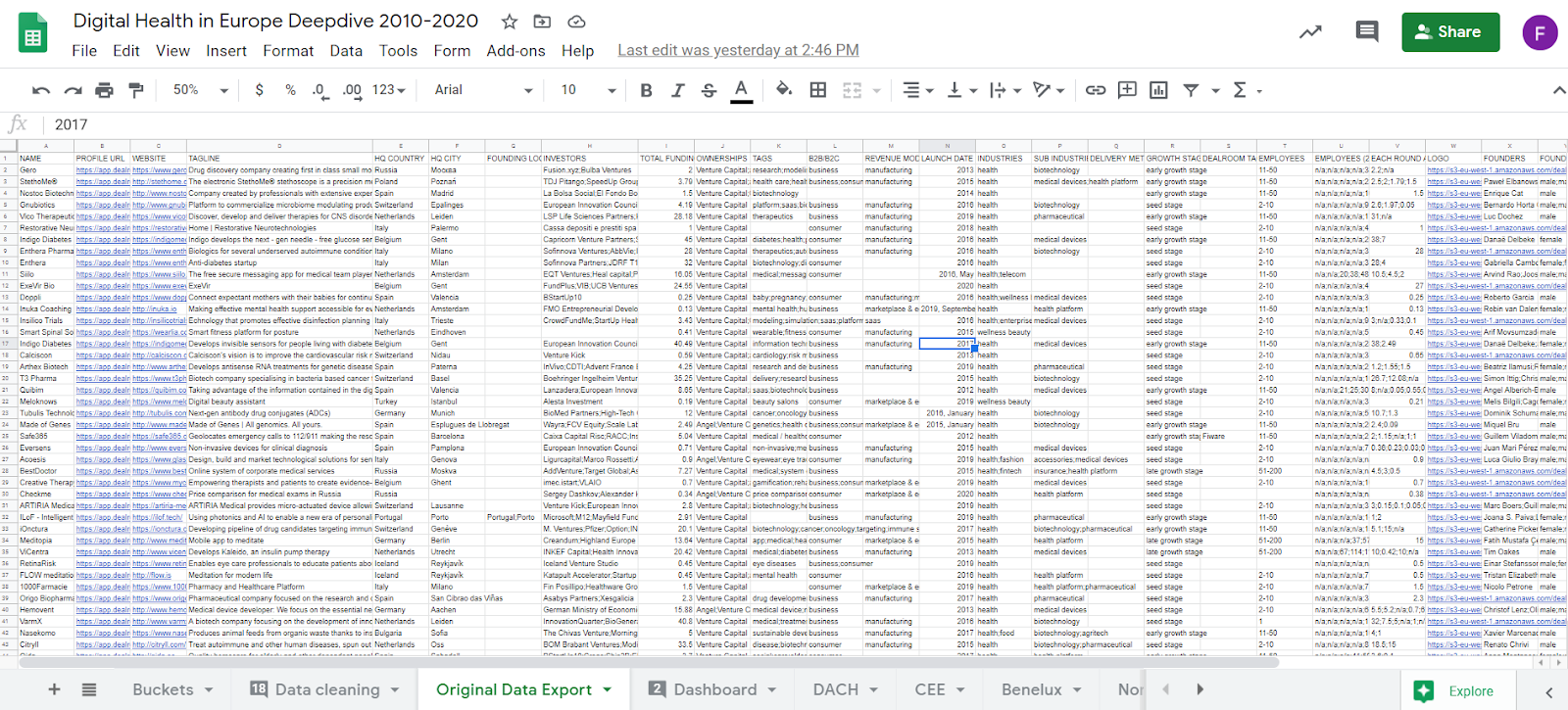

Building this sort of database is a mammoth project and it helps to be able to stand on the shoulders of giants. In our case, we pulled initial data from our friends at dealroom.co, using the following search criteria:

- Industries: Health; Wellness & Beauty

We missed a few companies that do not have either of these tags in Dealroom’s database but still operate in digital health. Wherever possible, we included them manually. - Geo-focus: Europe+

Beyond the EU, we include non-EU markets like the UK, Switzerland, Norway, Iceland, Russia, the Balkans, etc. - Year of Founding: Between 2010–2020

The 10-year range means we’re including both recently founded companies but also some older digital health scale-ups. - Funding: Minimum of €50k

This excludes unfunded and/or very young startups. We’ve analysed these companies separately and will eventually share our insights on these as well. Analysing this bunch takes longer because they include companies that:

- we’re still looking at for investment;

- are too young to classify;

- are not feasible investment targets (e.g. local SMEs with limited growth ambitions); have raised funding but chosen not to disclose the amount; and

- have closed rounds that don’t show up in the data because of a reporting lag for seed stage companies. Whenever we discovered startups that still fit the bill, we’ve tried to include them manually. If you feel your startup should be included in our database, drop us a line here!

- Funding round types: Angel, Convertible, Early VC, Grant, Growth Equity, Late VC, Seed, Series A-G.

- Ownership: Venture capital

This important limitation excludes startups that do not have at least one VC investor, such as purely strategic investments, spin-outs, and some angel rounds, etc. This selection is mainly motivated by our own investment focus as a VC fund, but it does mean that inappropriately tagged investors in Dealroom or startups that just raised an angel round may have missed the cut-off. We tried to include those anyway. - Company status: Operational

This was done in order to exclude acquired and defunct companies. This excludes some prominent exits, we’ll include and analyse those further down the line.

Data cleaning

The above filters left us with a dataset of 1599 companies. We then narrowed the data set down to 626 companies by zooming in on characteristics that we think are particularly interesting or relevant and excluding others. Specifically, we excluded startups with the following labels:

- Biotechnology and Pharma: “Wet” tech is not our focus, though as you’ll see we included all companies that produce software for use in life sciences.

- Cosmetics: We’ve looked at a number of cosmetics DTC models in the past, but these are usually pure consumer-companies without a digital health angle. We took a generous view here and only excluded very obvious non-health cases.

- Pet health: We love pet-tech, but decided to focus on human health for now.

- Insurance: Speedinvest’s Fintech team is far better placed to cover these.

- Cannabis: Sadly outside our investment guidelines.

- Medical devices: We excluded medical device companies whose main USP, IP and business model centers around certified medical devices. We kept companies that use off-the-shelf hardware or who use hardware as an enabler for a software-centered business model. On many edge-cases we took a generous view.

- A handful of miscellaneous startups that somehow slipped through these filters but had little to do with digital health.

- Companies whose founding members were no longer working at the company based on their Linkedin profile, or where we were unable to find anything of value online.

- Of course, we also added companies from our own deal flow that fit the above criteria, but were not in the original data-set!

Tagging for sub-verticals

The existing tags in the database, such as “platform”, “app”, “SaaS” and “care”, were often too broad for any meaningful analysis. Therefore, we introduced our own tagging system to systematize the remaining companies for our startup landscapes and deep dives.

We came up with buckets based on CB Insights’ Digital Health 150, their current gold standard in digital health startup mapping. First, we adapted their sub-vertical categories to better reflect the European market. We then assigned each startup to one or several of the following buckets according to their core sub-vertical focus or business model:

- Digital Therapeutics: Software that helps patients self-manage their conditions, usually over a longer period of time, with mostly light-weight professional medical support.

- Workplace Health: Health services or enabling tech for employers.

- Consumer Health: Lifestyle focused startups with broad B2C appeal, usually around fitness, nutrition, etc. As a separate sub-bucket we also tagged

- Direct to Consumer: D2C business models.

- Enabling Tech for Providers: Horizontal, back-end and business process tools for health providers, mostly B2B SaaS.

- Patient Engagement: Patient-interfacing and care management solutions that facilitate interactions between providers and patients.

- Clinical Trials & RWE: Startups focused on sourcing patients or data for pharma/life science R&D.

- Drug Discovery: All software related to drug discovery.

- Pharma Enablers: Software for pharma that is not related to R&D or sourcing evidence, for example solutions for supply chain management, commercial processes, sales tools, etc.

- On-Demand Generalist Care: Mostly telemedical primary care providers, usually focused on facilitating one-off, on-demand, generalist care. Often B2C, B2B or B2B2C.

- Specialized Virtual Care: Platforms that help patients comprehensively tackle a condition over time. Goes beyond a DTx and usually includes professional care along specialized care pathways, often focused on a subset of diseases / therapeutic needs. We also separately labeled the below uckets, which usually represent a subset of this category:

- Chronic Care: Focus on chronic patient populations, for example with cardiac issues, Diabetes, etc

- Mental Health: Focus on mental health issues, like anxiety, phobias, depression. Depending on the nature of the service, these can also be considered DTx’.

- Women’s Health: Focus on women’s health issues, like menopause, contraception, fertility,

- Family Health: Focus on kids and paediatric health, often in combination with family-wide issues.

- Men’s Health: Focus on men’s health, often including erectile dysfunction, hair-loss, etc.

- Screening & Diagnostics: startups that provide diagnostic software. This is a broad bucket that includes home testing, AI-enabled medical imaging, digital pathology, and a ton of companies applying ML/AI to radiological output.

- Sexual Health: Everything related to sex, both medical and casual focused, and we usually tagged womens’/mens’ health on top.

- Elderly care: Solutions providing care and services around ageing populations and elderly people.

- Hardware: Proprietary hardware and companies with a strong hardware USP that, in contrast to traditional medical device players, have a clear software-enabled or -centered business model.

For each company we assigned multiple and primary tags:

- Multi-tagging means that, for example, a workplace mental health solution like Spill Chat would have been tagged for both “Workplace Health” and “Mental Health”. Likewise, a startup like Kaia Health was multi-tagged for “Chronic Patient Care”, “Specialized Virtual Care” and “Consumer Health”.

- Primary tagging means that Kaia was assigned a “Digital Therapeutics” label as the overarching category, and Spill was put in the “Mental Health” bucket.

Geo-allocation

To help split the companies into broader geographies, we assigned them to regions broadly aligned with the EU’s EuroVoc standard. The regions we included are: