Understanding the New Early-Stage Funding Cycle in Europe

The funding path has been clear... until now.

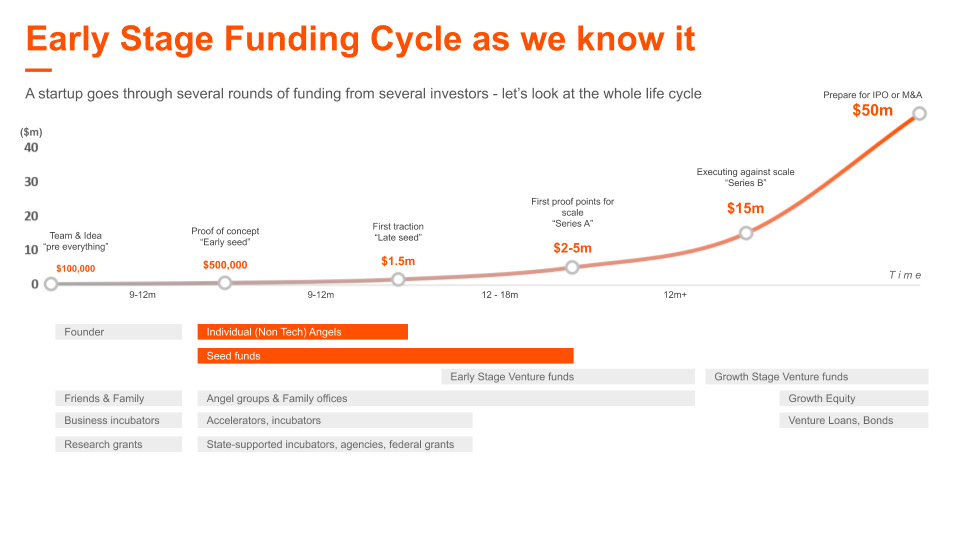

The traditional early-stage funding cycle has always been pretty straightforward. Founders started with money from friends and family, savings, or grants. After some fine-tuning of their product idea and business model, they raised their first institutional round with either a seed investor, business angels, and/or some family offices. Maybe they applied for an accelerator program.

With this firm foundation, they built the first product and hopefully attracted clients and found product-market fit. This, in most cases, led to a Series A round, and ideally, growth, later stage investors, and an eventual exit or IPO. This textbook journey took, on average, eight to ten years and has been the accepted way of things for quite some time. But things are changing.

Why is this happening? How is it impacting the early-stage funding cycle in Europe? Who’s benefiting?

Let’s start by digging into what’s driving this “new normal.”

Trend #1: There is just more money🤑

Everybody’s heard stories or read articles about ever bigger Seed (and A, B, C, etc.) rounds in Europe. Series A rounds, which just a couple years ago averaged around €5 million, are often much larger today. The reason? Competition among investors for the best startups has dramatically increased.

Longer value incubation times

Investors are pouring more money into startups because in recent years money has continued to pour out, i.e. they’re getting great returns. So companies like Airbnb, Uber, etc. no longer have to rely on public money, and they can stay private longer, as outlined in our post from last year.

According to Morgan Stanley Research, in 2017 alone, companies raised $3.0 trillion in private markets and $1.5 trillion in public markets. In fact, companies have raised more money in private markets versus public markets in every year since 2009.

The result, the average time to IPO has increased to eleven years, and exits, either by being sold to a strategic buyer or private equity firm, or via IPO, happen at much higher valuations that no one would have imagined (or predicted) twenty years ago.

Where there’s money to be made…

Investors appear. They are looking for returns and don’t want to miss out on this value creation in private markets! And if you, as an LP, invest in the right VC and private equity firms, then you can achieve great returns (but only if you invest in the right firms).

As a result, according to a survey by Morgan Stanley, close to 40% of surveyed institutional investors plan to further increase investments in alternative assets, including here in Europe.

It’s no surprise then that, since 2014, the number of new funds raised has grown significantly. That number peaked in 2018 (with 2020 stats still incomplete), but the total amount of Seed and Series A money raised continues to increase. In 2020, that equates to €13.1 billion in capital, so far.

Lakestar’s $735m fund and Atomico’s $820m fund are perfect examples. The growth of the number of funds may be decreasing, but there’s still a ton of capital in the market.

There’s a lot of capital, but less demand.

So an increasing number of Seed and Series A funds have ever more capital at their disposal. The money is there. But what about the demand? Are there enough companies actually seeking venture capital in Seed and Series A?

We can see the demand for capital rapidly increased up until 2014. More and more Seed rounds were happening at the same time as more startups were being founded. But this has stopped and basically stagnated. As the rules of supply and demand dictate, that has led to great competition between investors, and therefore higher prices. The average post-money valuation for Seed and Series A rounds almost tripled from 2010 to 2020.

These lucky fewer startups are now being fought over, driving up investment interest and creating larger rounds at higher valuations.

I assume this is not breaking news. But I think it’s important to lay the foundation before we discuss just how much the early-stage funding cycle has changed.

Trend #2: Non-traditional players are entering the field 🆕

Is VC the right investment for me? What are the returns? How quickly will I see money in the bank? Are there other options?

Investors and corporates have been asking questions like these for years. VC funds, as we all know, are not the only option out there. It’s also not the right option for everyone. Interest in alternatives has led to the rise of new investment models, especially over the past five years, and VC now comes in many forms.

Here are, in my opinion, a few of the most important players we’re seeing in the market:

Scout funds 🔍

Due to increased competition, traditional Series A and later-stage investors began looking for deal flow very early on — mostly at universities and other important tech hubs. Whether by funding student teams directly, like First Round Capital’s dormroom fund, or by teaming up with venture partners to do direct pre-seed investments, as is the case with the Atomico Angel Program, the goal is to get deals before others do.

Angels are becoming more professional 📑

As the European ecosystem matured due to impressive exits, so did angel investors. There are now some very experienced angels and angel syndicates in the most important European startup hubs, and they now have deeper pockets to do bigger tickets. So it’s now common to see them throughout pre-Seed to Series A.

With companies like AngelList on the scene, a new industry is developing. It offers many more people the chance to invest in startups via managed funds. Spearhead is another example, where founders get money and professional support to participate in angel tickets.

Micro VCs 🎙️

Micro VCs are a new wave of smaller funds (up to €50M), often based on a strong investment thesis, in pre-Seed, Seed or Series A that tend to focus on a specific geographical area and/or focus (e.g. SaaS).

Later-stage funds are investing earlier 💰

What has been common practice in the US for quite some time — especially in the Bay Area — is now also slowly coming to Europe. Big household names in VC are competing with seed funds much earlier.

Either through scout funds or dedicated seed teams within the firms, these funds now have the potential to finance a company through the whole business lifecycle (and often do).

Corporate VCs 💼

Corporates are increasingly interested in investing in early-stage startups building the latest innovations in their industries. Rather than funding other funds, they’re doing direct tickets, often very early ones, via their own venture arms. And it’s not just giant corporations, even smaller corporates are getting into the game.

So what’s the bottom line?

All of these investors are now fighting to get first access to the best founders before everyone else, and they want to increase their ownership stake in every deal. This ultimately leads to a fear of missing out among investors, less cooperation and syndication on deals, resulting in very fast follow-on rounds initiated by investors determined to get a stake in a great deal.

So, let’s recap:

- More funding available has led to startups not being required to go public as quickly (or never), resulting in much larger rounds.

- Investors don’t want to miss out on the great returns we’ve been seeing in private markets.

- The increase of capital, while the number of new startups to invest in has decreased, causing a steady rise in valuations.

- With so many looking for a place to put their money, we’ve seen a wave of new investors, increasing competition between traditional and non-traditional investors even further.

All of this fighting for a piece of Europe’s very best startups creates a lot of value in the ecosystem. Those lucky enough to be fought over will now benefit from the Early-Stage Funding Cycle 2.0.

What does this funding cycle look like? How do traditional VC and new alternative asset players fit into the puzzle? And what can founders expect when fundraising?

Here’s what you’ve been waiting, our hypothesis:

Is this what you’re seeing, too? Or do you have another perspective on the future of early-stage funding in 2021 and beyond?

We’d love to hear your thoughts and market observations!

Speedinvest is a leading pan-European, early-stage venture capital firm. Our portfolio includes Wefox, Bitpanda, TIER Mobility, GoStudent, Curve, CoachHub, Schüttflix, TourRadar, Adverity, and Twaice. Sign up for our newsletters to get our exclusive content delivered straight to your inbox.

.svg)